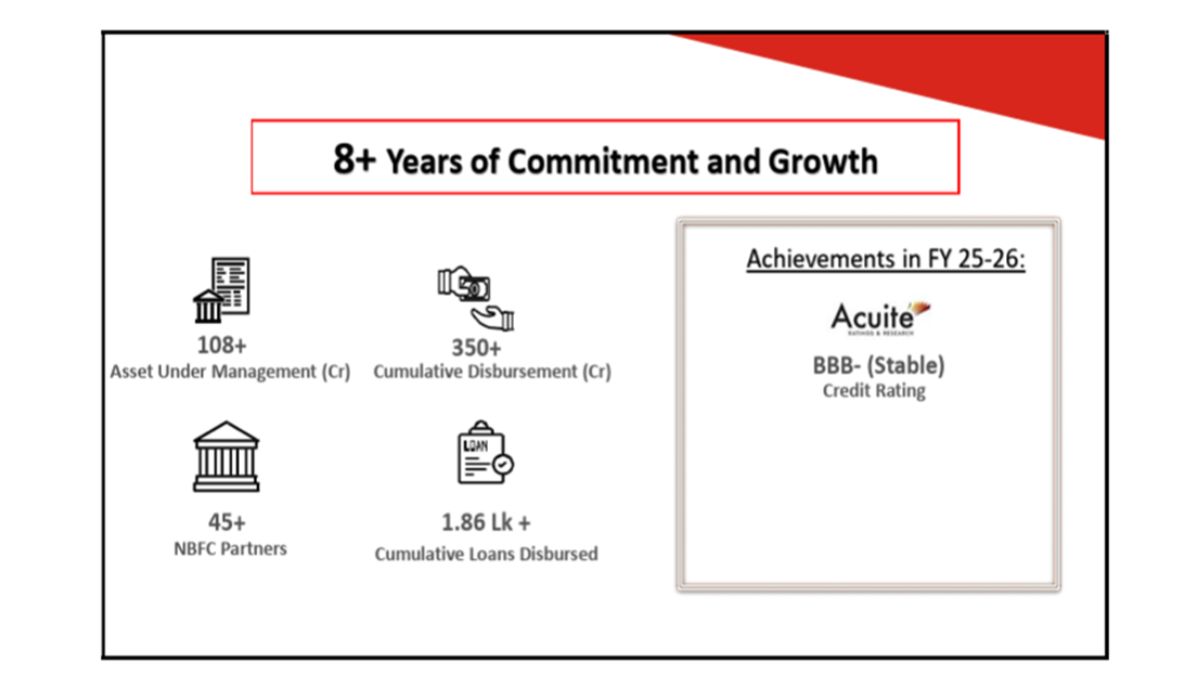

Surat (Gujarat) [India], March 21: IBL Finance Ltd (NSE – IBLFL) a fintech-driven Non-Banking Financial Company has secured a LONG-TERM INVESTMENT GRADE rating of BBB- (Triple B Minus) with a Stable Outlook by the rating agency Acuité Ratings & Research Limited.

This achievement reflects the Company’s strong governance standards, prudent risk management practices, sound financial discipline, and robust compliance framework. The rating reinforces our credibility within the financial ecosystem and marks an important milestone in strengthening our market position and long-term growth strategy. With this rating, IBL Finance Limited is well-positioned to access capital at competitive rates, accelerate strategic investments, and further strengthen its leadership in the fintech-enabled lending space.

Key Strengths

- Healthy Capital Structure

IBL Finance Limited maintains a strong capital position supported by a healthy net worth and comfortable capital adequacy levels. The Company has a net worth of ₹ 59.90 Crore as on September 30, 2025. IBLFL is listed on the NSE Emerge and successfully raised ₹ 33.40 Crore through its IPO in January 2024, strengthening its capital base to support future growth.

The Company’s gearing remained comfortable at 0.62x as on September 30, 2025, indicating adequate headroom for further borrowings. Additionally, the Company maintains a strong Capital to Risk-Weighted Assets Ratio (CRAR) of 57.27% as on September 30, 2025, significantly above regulatory requirements.

Post IPO, the promoters and the promoters group continue to hold approximately 63% shareholding, reflecting continued promoter commitment, while the remaining shareholding is held by public investors.

- Strong and Diversified Debt Resource Mix

The company has a well-diversified resource mix for debt raising. As of September 2025, approximately 21% of the total borrowings are raised through NCDs, while around 79% are sourced from Financial Institutions (FIs). Going forward, the company intends to further diversify its borrowing profile by raising funds through multiple channels, including NCDs, loans from FIs, and bank borrowings, with the objective of optimizing borrowing costs and maintaining a well-structured debt resource mix.

- Stable Asset Quality

The Company is engaged in Financial Institution (FI) lending and personal loans, with FI lending forming the core of its portfolio. As of September 30, 2025, approximately 90% of the Company’s AUM comprised FI lending to NBFCs (Secured), while the remaining portfolio consisted of personal loans.

As of September 30, 2025, the Company reported Gross NPA (GNPA) of 2.71% and Net NPA (NNPA) of 2.44%, indicating stable asset quality, compared to GNPA of 2.54% and NNPA of 1.99% as on March 31, 2025.

- Strategic Allocation of Lending Across Product Segments

The company has diversified its lending portfolio across multiple product segments through financing to Financial Institutions (FIs). As on September 2025, the portfolio (end use wise) is well distributed with 39.14% in Personal Loans, 15.65% in Business Loans (secured & unsecured), 12.00% in Vehicle Loans, 10.31% in Consumer Loans, 9.86% in Loan Against Property (LAP), 7.88% in Microfinance (MFI), and 5.16% in Gold Loan.

Financial Performance

Over the past few years, the Company has demonstrated strong and consistent financial growth with clear year-wise improvements across all key parameters. The Net Worth has increased significantly from ₹20.67 crore in FY 2022–23 to ₹59.90 crore as of September 2025, reflecting a robust growth of 190%. Similarly, Assets Under Management (AUM) have expanded sharply from ₹14.61 crore in FY 2022–23 to ₹94.13 crore in September 2025, marking an impressive growth of 544%, indicating strong business expansion and customer acquisition. On the profitability front, Profit Before Tax (PBT) has improved from ₹2.86 crore in FY 2022–23 to ₹2.99 crore in FY 2024–25, while Profit After Tax (PAT) has remained healthy, growing from ₹2.05 crore in FY 2022–23 to ₹2.36 crore in FY 2024–25, and standing at ₹1.24 crore for the half year ended FY 2025–26. In terms of asset quality, the Company has shown notable improvement with Gross NPA reducing from 5.19% in FY 2022–23 to 2.71% in September 2025, and Net NPA declining from 3.94% to 2.44% over the same period. Overall, the year-wise performance reflects a well-balanced growth strategy supported by improving profitability and strengthening asset quality.

About IBL Finance Limited

IBL Finance Limited (IBLFL), established in 2017, represents a new generation of financial services innovation in India. As a fintech-driven Non-Banking Financial Company (NBFC) registered with the Reserve Bank of India (RBI) and listed on the NSE Emerge platform, stand at the intersection of traditional financial expertise and cutting-edge digital technology.

The Headquartered in Surat, Gujarat—one of India’s most dynamic business hubs—IBL Finance has established itself as a trusted financial partner for diverse customer segments. Our comprehensive product portfolio serves individuals seeking personal financial solutions and NBFCs looking for institutional funding partnerships. This diversified approach ensures that company remain resilient across market cycles while delivering consistent value to their stakeholders.

Since commencing operations in 2018, IBL Finance has achieved remarkable milestones: disbursing over ₹350+ crores in loans and serving 1.86+ lakh customers across India. This track record demonstrates company ability to scale operations efficiently while maintaining asset quality and customer satisfaction. Company’s pan-India presence ensures that it can serve customers wherever they operate, from metropolitan cities to tier-2 and tier-3 towns.

Disclaimer:Certain statements in this document that are not historical facts are forward looking statements. Such forward-looking statements are subject to certain risks and uncertainties like government actions, local, political, or economic developments, technological risks, and many other factors that could cause actual results to differ materially from those contemplated by the relevant forward-looking statements. IBL Finance Ltd. will not be in any way responsible for any action taken based on such statements and undertakes no obligation to publicly update these forward-looking statements to reflect subsequent events or circumstances.